State of Revenue 2026:

Selling the Platform: Why Most Companies Struggle and What the Best Ones Do Differently

Introduction

The platform sale has become the defining commercial challenge for a generation of technology companies. But it did not arrive without warning. Over the last decade, many companies built their go-to-market around focused point solutions, then grew through acquisition — adding adjacent products to the portfolio, increasing the bundle, and telling a progressively broader story to customers.

For a while, this works. New products get added to existing contracts. A handful of flagship customers buy into the vision early. Revenue grows. But over time, two things tend to happen. The cost of providing an increasingly complex bundle starts to erode margins. And the incremental value customers get from adding another product to the mix begins to plateau — because the real value of a platform only comes from genuine integration, not co-packaging. At that point, the commercial imperative shifts. The company needs customers not just to buy more products, but to commit to the platform as a whole.

That is a categorically harder sell, and most organizations discover this the hard way.

"Moving to a platform approach was difficult to execute internally — it took a long time and sales lost focus or became too busy to see it through." — Survey respondent

To understand what separates companies that manage this transition from those that do not, Insight Revenue surveyed approximately 50 companies and followed up with qualitative interviews. The market context gives the research its urgency: the SaaS market alone is worth around $500 billion in annual revenue, and the top 20 vendors control more than half of it. Winner-takes-all dynamics are intensifying especially with the rapid integration of AI into technology and service offerings. Becoming overwhelmed with options and higher scrutiny on spend, it is no surprise, vendor rationalization is a top buyer priority in 2026 — organizations want fewer, deeper relationships. For most sellers, the platform sale is no longer aspirational. It is a matter of survival.

The finding that most surprised us was not about capability gaps or market conditions:

The platform sale is not failing because buyers are uninterested. It is failing because sellers are not answering the right questions.

Before buyers will commit to anything beyond a limited pilot, they need credible answers to three specific questions:

- Can it actually be done? Buyers need to be inspired — not just told it works.

- Is it worth the disruption? Buyers need to work out the impact for themselves.

- Will we survive the journey? Buyers need a clear, believable path through implementation.

Companies that learn to answer these questions — consistently, not just occasionally — win the platform sale. Those that cannot will keep seeing the same pattern: enthusiasm that does not convert, pilots that do not expand, and proposals that die in procurement.

Why Platform Selling Is Different

Platform selling is not a harder version of a product sale. It is a different activity, and treating it as an extension of what worked before is one of the most common mistakes we observe. Four things make it structurally different.

More stakeholders, with more at stake

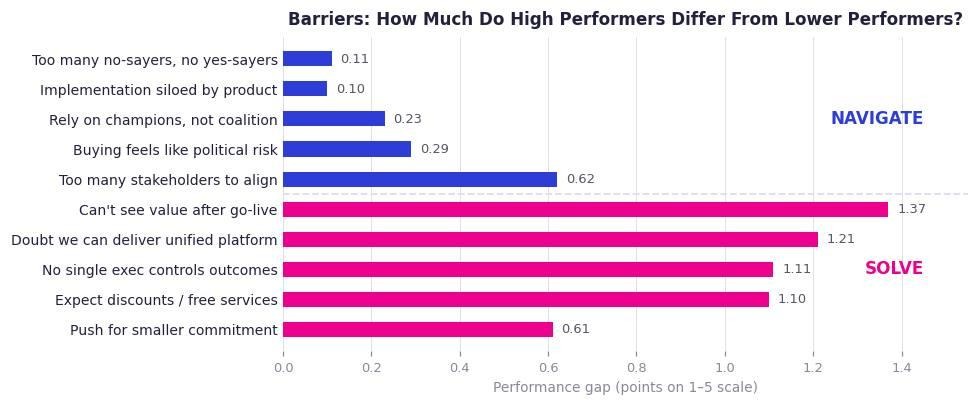

A product sale typically involves a primary buyer, a user group, and procurement. A platform sale adds the functions the platform will change: operations, IT, finance, HR, and usually the C-suite. Our research found that the ownership problem — no single executive controls all the outcomes being promised — is the most common challenge in our data, felt almost universally regardless of how well the company is performing overall.

The customer has to change how they work

A product can be added without disrupting much. A platform requires the customer to do things differently. The sale is therefore not just a commercial decision — it is a change management decision. Buyers are not just evaluating whether the solution is good. They are evaluating whether their organization can survive the transition to it.

The seller has to prove something that has not happened yet

Product demos are relatively straightforward. Platform sales involve promising an integrated outcome that is harder to demonstrate in advance. Skepticism about whether the vendor can actually deliver the whole as a unified solution — not just the component parts — is one of the most significant deal-killers in our data.

"What we sell is very complex, so it scares people. You have to slow down and make sure the key concepts are understood." — Survey respondent

The standard sales playbook works against you

Land and expand. Lead with a use case. Run discovery, present the demo, handle objections. These motions were optimized for a product sale. Applied to a platform sale, they tend to produce exactly the wrong outcome: smaller deals, narrower engagement, and a customer who still sees you as a point-solution vendor — which 48% of respondents acknowledged their customers still believe them to be.

"Too in the weeds, too feature focused, demos too technical — we really struggle with ROI and business case creation, urgency beyond discounts." — Survey respondent

What the Research Shows

Our research identified six categories of barriers that limit platform deal progress. They are not all equally addressable, and understanding the difference is the starting point for knowing where to invest.

The barriers everyone faces

Ownership and consensus

The most pervasive finding in our research is also the most intractable. High-performing and lower-performing companies report almost identical difficulty here:

67% agree: "too many people can say no, and no one can say yes"

61% agree: "we rely on champions rather than a real coalition"

59% agree: "too many stakeholders to keep aligned"

High performers score almost the same as their peers on all three items. This is not a problem that better selling eliminates — it is a structural feature of platform deals. Companies that wait for a single clear decision-maker before advancing will wait a long time.

The champion trap is a specific version of this worth naming. A champion who believes in the platform but lacks the organizational authority to move it forward is one of the most common reasons deals stall.

"Our main contact, who was a champion of the product, did not have enough power to persuade their boss to buy." — Survey respondent

Political risk

More than half of respondents (54%) agree that buying a platform feels like a political risk for the buyer — career exposure, internal politics, the fear of sponsoring a failed transformation. High performers are only marginally better at managing it. The best sellers do not try to argue buyers out of this. They reduce the perceived risk of the decision itself.

Where high performers pull away

Commercial architecture: the beachhead trap

When customers push back on a full platform commitment — asking for a smaller scope, different payment terms, a longer pilot — the natural response is to accommodate. Our data suggests this is the wrong instinct.

The pressure to disaggregate is real and rational — customers are managing genuine risk. What separates high performers is that they do not interpret that pressure as a signal to concede. They interpret it as a question that has not yet been answered.

When a customer asks to start small, they are almost always asking one of the three foundational questions in disguise. Accepting a beachhead does not answer those questions — it defers them, usually permanently.

"A senior stakeholder jumped in and asked for the project to be split into two phases — so they didn't take the bigger solution, just a fraction of it, to get started." — Survey respondent

Notably, high performers are more likely than peers to say that "land now, expand later" is their default motion (57% vs. 40%). This is not a contradiction — it reflects greater awareness of the trap. They feel the pull and resist it deliberately.

"Didn't eat our own dog-food — took shortcuts — fell foul of the RFP process — too easily added to a line-up for the purpose of gathering quotes instead of following our own qualification process." — Survey respondent

Delivery credibility

Customer doubt that a vendor can deliver the full platform as an integrated whole — not just the individual components — is a significant barrier across the sample. High performers have largely closed this gap through more rigorous pilot design, stronger references, and a post-sale experience that produces visible value quickly.

Post-sale value visibility

The largest single performance gap in our data has nothing to do with how companies sell. It is about what happens after the deal closes. On whether customers can easily see the value they are getting after go-live, high performers score 1.86 out of 5 (lower is better on this barrier item), while lower performers score 3.23 — a gap of 1.37 points, larger than any other item in the survey.

This reframes the platform sale in an important way. The behaviors that most directly separate high performers from the rest are not pre-sale. Getting to signature is necessary but not sufficient.

"A lack of perceived value — generally driven by under or improper utilization of the platform." — Survey respondent

Customer-side barriers

Two additional barriers attract broad agreement and affect how the conversation needs to be framed:

- 70% say customers need more peer adoption and proven references before committing. Nobody wants to be first.

- 62% say customers agree they should innovate — but believe now is not the right time. Not active rejection, but indefinite deferral.

The Three Questions Buyers Need Answered

Every barrier we identified maps back to one of the three questions below. Sales organizations that orient their approach around these questions — rather than around features, demos, or ROI models — consistently outperform those that do not.

When any one of these goes unanswered, the deal does not close — it shrinks. Customers ask for something smaller and safer, pilots multiply without converting, and sellers find themselves back in a product sale. Getting back to a platform conversation from there is rare.

Organizing for Complexity

The three questions are not the individual seller's problem alone to solve. The organizations that answer them consistently have built infrastructure that makes it possible — reducing the burden on sellers so they can focus on the work that actually requires human judgment.

High performers invest in four things at the structural level.

1. Getting incentives right

Compensation systems that reward quick wins undermine the platform sale. Sellers measured primarily on quarterly attainment will default to the path of least resistance — which is always the product sale. This is a rational response to how they are measured, not a character failure. Addressing it is a prerequisite, but 46% of respondents acknowledge their incentives are still misaligned.

2. A pilot process that proves the business case

The absence of references is one of the most significant impediments to platform sales. Pilots are the natural answer — but most fail because they end up proving the technology rather than the business case. A technically successful pilot that does not produce measurable business impact does not advance the deal. It delays the same conversation.

High performers design pilots differently:

- Pilots are a scarce resource, not a giveaway. Offered selectively, to customers who have demonstrated genuine strategic intent and organizational readiness.

- KPIs are agreed before the pilot begins, tied to hard outcomes. Revenue, cost reduction, or quantifiable risk — not engagement metrics. The baseline is set in advance so the before-and-after contrast is unambiguous.

- Full implementation is the default, with opt-out rather than opt-in. This disqualifies customers who want a proof of concept but not a genuine transformation — and creates a sense of inevitability that makes the larger commitment feel like a natural next step.

3. A redesigned sales motion

Platform selling requires a more fluid sales motion than most organizations have built. The stages are the same — what happens within them is substantially different.

The biggest shifts are in the middle stages. Explore is about shaping the problem, not just uncovering it. Align is about building a coalition, not managing a single buyer relationship. Both require different conversations and longer time horizons than most product-era sales processes were designed for.

4. Infrastructure for internal coordination

One of the least-discussed differences between high and lower performers is how they coordinate internally around complex deals. Pulling in the right experts at the right time is a persistent weak point — only 39% of companies rate themselves above average at it.

In most organizations, sellers working on a complex deal have to beg and borrow time from colleagues in pre-sales, solution architecture, customer success, and implementation. The coordination that happens depends on personal relationships and goodwill — not process.

"Due to M&A, too many silos — not efficient enough at the moment." — Survey respondent

High performers fix this by creating a formal mechanism for assembling the right internal expertise around deals of sufficient size and complexity — not an additional pipeline review, but a structured forum where deal teams and specialists work through a specific customer opportunity together, using a shared customer value roadmap as the common working document.

This also closes the post-sale gap. The handoff between sales and implementation — one of the most dangerous moments in a platform deal — becomes a continuation of a shared process rather than a cold transfer of ownership.

Individual Behaviors That Distinguish High Performers

Organizational infrastructure creates the conditions. But the sale depends on what individual sellers do in the room.

One finding worth noting upfront: across all nine dimensions, the average self-rating sits between 3.0 and 3.4 out of 5. No single behavior stands out as a clear organizational strength. The gaps between high and lower performers are modest on most pre-sale items — but they open up meaningfully on the post-sale behaviors, consistent with everything else we found.

Three behavioral differences distinguish high performers.

1. Stakeholder mapping before anything else

The instinct in most sales processes is to get to the decision-maker quickly. High performers do something different first: they map the full stakeholder landscape.

Not just the formal buying group — but who is affected by the purchase, who owns the problem, who can veto from outside the room, who might become an informal champion or blocker. They profile individuals: visionary or risk-averse, ally or sceptic, what their track record suggests about how they respond to change.

This is not optional groundwork. Without it, you cannot surface the right risks with the right people, or build a business case that lands with the people who matter.

"Multi-threading, finding mobilisers, being more prescriptive about what a client should do vs. what they want to do." — Survey respondent

2. Raising uncomfortable questions early

The instinct in a complex, high-stakes deal is to present the cleanest possible picture. High performers do the opposite: they surface the awkward questions before the customer does.

The most intractable barriers to platform deals are almost never technical. They are internal to the customer: cultural norms, political relationships, organizational inertia. Sellers who wait for these to surface on their own find them emerging late in the process, when they are hardest to recover from.

"If we've decided there's a need, I'm also going to make sure they address the need," one respondent put it. "If I walk away now, I'm never going to place a solution with them." Surfacing risk early requires both courage and genuine knowledge of what a real implementation involves.

3. A shared business case

The business case is the mechanism through which all three buyer questions get answered in one document: whether it can be done (implementation roadmap and references), whether it is worth it (financial model and cost of inaction), and whether the customer will survive the journey (change management and risk plan).

The critical word is shared. A business case that a seller presents to a buyer is a proposal. One developed together is closer to a commitment. High performers invest in the co-creation process accordingly.

The best business cases go beyond a single-point ROI to present ranges and scenarios — including the cost of doing nothing and the cost of a DIY alternative. In an environment where buyers conduct their own AI-assisted research before every major purchase, an honest range of scenarios is harder to dismiss than a deterministic model.

"When business objectives are known and aligned to the sales message, and the right people are in the room, and the client is properly qualified — our close ratios are phenomenal." — Survey respondent

Conclusions

The platform sale is widely framed as a product problem — a matter of having the right capabilities — or a pricing problem. Our research suggests the real constraint is elsewhere: a gap in sales strategy and organizational capability, specifically the ability to answer three questions that buyers need answered before they will commit to anything more than a proof of concept.

Most organizations describe the value of a full implementation compellingly. But they fail to address the foundational questions around feasibility, impact, and risk — and in the absence of answers, buyers do what any rational actor would do. They ask for something smaller.

The companies that manage this transition invest in the right organizational infrastructure: disciplined pilot design, a redesigned sales motion, aligned incentives, and a formal mechanism for assembling internal expertise around complex deals. Individually, they develop sellers who can navigate complexity rather than just describe their product: who map stakeholders before advancing, surface risks before they surface themselves, and build business cases collaboratively rather than presenting them.

For sales leaders, this reframes the capability agenda. The platform sale does not reward sellers who know more. It rewards sellers who can move across stakeholder groups, connect commercial and operational threads, and hold productive tension with buyers who are skeptical of both the promise and the disruption involved in acting on it.

The stakes for buyers are real. A failed platform implementation can damage a budget and end a career. Sellers who show up prepared to de-risk the decision — rather than just close it — earn a different kind of trust. That trust is what every large platform deal we observed in our research was built on.

How Insight Revenue Can Help

The barriers described in this research are real, but they are not insurmountable. Insight Revenue works with commercial organizations to build the strategy, structure, and individual capabilities needed to win platform deals consistently.

Our work starts with diagnosis. Using the same research framework that underpins this report, we benchmark your organization against peers across the six barrier categories — giving your leadership team a clear picture of where you are navigating well and where you are conceding ground unnecessarily.

From there, we install the BRIDGE Customer Value Roadmap: our structured methodology for managing complex platform deals from first conversation to successful implementation. BRIDGE, which is part of our ´Insight to Value´ sales model, gives sellers, deal teams, and internal experts a shared language and a common process:

- Blueprint the customer's strategy, goals, and stakeholder landscape — before advancing the deal.

- Reframe with insight — introducing perspectives that shift how the customer sees their situation and the cost of staying where they are.

- Illustrate impact — building a business case around the customer's own metrics, including cost of inaction and realistic implementation scenarios.

- Defuse obstacles — surfacing the political, organizational, and operational barriers early, when there is still room to address them.

- Gauge the options — mapping the competitive landscape honestly, including the cost and risk of doing nothing or building in-house.

- Execute a joint plan — a shared roadmap that answers the third foundational question: will we survive the journey?

BRIDGE also provides the structure for the internal coordination forum described in this report. When deal teams work through the roadmap together, the handoff between sales and implementation becomes a continuation of a shared process. Customers experience this as continuity, not a change of ownership.

The result is a commercial organization that does not just sell the platform. It delivers on it.

Download the full report below.

Download the free resource

State of Revenue 2026:

Selling the Platform: Why Most Companies Struggle and What the Best Ones Do Differently

Introduction

The platform sale has become the defining commercial challenge for a generation of technology companies. But it did not arrive without warning. Over the last decade, many companies built their go-to-market around focused point solutions, then grew through acquisition — adding adjacent products to the portfolio, increasing the bundle, and telling a progressively broader story to customers.

For a while, this works. New products get added to existing contracts. A handful of flagship customers buy into the vision early. Revenue grows. But over time, two things tend to happen. The cost of providing an increasingly complex bundle starts to erode margins. And the incremental value customers get from adding another product to the mix begins to plateau — because the real value of a platform only comes from genuine integration, not co-packaging. At that point, the commercial imperative shifts. The company needs customers not just to buy more products, but to commit to the platform as a whole.

That is a categorically harder sell, and most organizations discover this the hard way.

"Moving to a platform approach was difficult to execute internally — it took a long time and sales lost focus or became too busy to see it through." — Survey respondent

To understand what separates companies that manage this transition from those that do not, Insight Revenue surveyed approximately 50 companies and followed up with qualitative interviews. The market context gives the research its urgency: the SaaS market alone is worth around $500 billion in annual revenue, and the top 20 vendors control more than half of it. Winner-takes-all dynamics are intensifying especially with the rapid integration of AI into technology and service offerings. Becoming overwhelmed with options and higher scrutiny on spend, it is no surprise, vendor rationalization is a top buyer priority in 2026 — organizations want fewer, deeper relationships. For most sellers, the platform sale is no longer aspirational. It is a matter of survival.

The finding that most surprised us was not about capability gaps or market conditions:

The platform sale is not failing because buyers are uninterested. It is failing because sellers are not answering the right questions.

Before buyers will commit to anything beyond a limited pilot, they need credible answers to three specific questions:

- Can it actually be done? Buyers need to be inspired — not just told it works.

- Is it worth the disruption? Buyers need to work out the impact for themselves.

- Will we survive the journey? Buyers need a clear, believable path through implementation.

Companies that learn to answer these questions — consistently, not just occasionally — win the platform sale. Those that cannot will keep seeing the same pattern: enthusiasm that does not convert, pilots that do not expand, and proposals that die in procurement.

Why Platform Selling Is Different

Platform selling is not a harder version of a product sale. It is a different activity, and treating it as an extension of what worked before is one of the most common mistakes we observe. Four things make it structurally different.

More stakeholders, with more at stake

A product sale typically involves a primary buyer, a user group, and procurement. A platform sale adds the functions the platform will change: operations, IT, finance, HR, and usually the C-suite. Our research found that the ownership problem — no single executive controls all the outcomes being promised — is the most common challenge in our data, felt almost universally regardless of how well the company is performing overall.

The customer has to change how they work

A product can be added without disrupting much. A platform requires the customer to do things differently. The sale is therefore not just a commercial decision — it is a change management decision. Buyers are not just evaluating whether the solution is good. They are evaluating whether their organization can survive the transition to it.

The seller has to prove something that has not happened yet

Product demos are relatively straightforward. Platform sales involve promising an integrated outcome that is harder to demonstrate in advance. Skepticism about whether the vendor can actually deliver the whole as a unified solution — not just the component parts — is one of the most significant deal-killers in our data.

"What we sell is very complex, so it scares people. You have to slow down and make sure the key concepts are understood." — Survey respondent

The standard sales playbook works against you

Land and expand. Lead with a use case. Run discovery, present the demo, handle objections. These motions were optimized for a product sale. Applied to a platform sale, they tend to produce exactly the wrong outcome: smaller deals, narrower engagement, and a customer who still sees you as a point-solution vendor — which 48% of respondents acknowledged their customers still believe them to be.

"Too in the weeds, too feature focused, demos too technical — we really struggle with ROI and business case creation, urgency beyond discounts." — Survey respondent

What the Research Shows

Our research identified six categories of barriers that limit platform deal progress. They are not all equally addressable, and understanding the difference is the starting point for knowing where to invest.

The barriers everyone faces

Ownership and consensus

The most pervasive finding in our research is also the most intractable. High-performing and lower-performing companies report almost identical difficulty here:

67% agree: "too many people can say no, and no one can say yes"

61% agree: "we rely on champions rather than a real coalition"

59% agree: "too many stakeholders to keep aligned"

High performers score almost the same as their peers on all three items. This is not a problem that better selling eliminates — it is a structural feature of platform deals. Companies that wait for a single clear decision-maker before advancing will wait a long time.

The champion trap is a specific version of this worth naming. A champion who believes in the platform but lacks the organizational authority to move it forward is one of the most common reasons deals stall.

"Our main contact, who was a champion of the product, did not have enough power to persuade their boss to buy." — Survey respondent

Political risk

More than half of respondents (54%) agree that buying a platform feels like a political risk for the buyer — career exposure, internal politics, the fear of sponsoring a failed transformation. High performers are only marginally better at managing it. The best sellers do not try to argue buyers out of this. They reduce the perceived risk of the decision itself.

Where high performers pull away

Commercial architecture: the beachhead trap

When customers push back on a full platform commitment — asking for a smaller scope, different payment terms, a longer pilot — the natural response is to accommodate. Our data suggests this is the wrong instinct.

The pressure to disaggregate is real and rational — customers are managing genuine risk. What separates high performers is that they do not interpret that pressure as a signal to concede. They interpret it as a question that has not yet been answered.

When a customer asks to start small, they are almost always asking one of the three foundational questions in disguise. Accepting a beachhead does not answer those questions — it defers them, usually permanently.

"A senior stakeholder jumped in and asked for the project to be split into two phases — so they didn't take the bigger solution, just a fraction of it, to get started." — Survey respondent

Notably, high performers are more likely than peers to say that "land now, expand later" is their default motion (57% vs. 40%). This is not a contradiction — it reflects greater awareness of the trap. They feel the pull and resist it deliberately.

"Didn't eat our own dog-food — took shortcuts — fell foul of the RFP process — too easily added to a line-up for the purpose of gathering quotes instead of following our own qualification process." — Survey respondent

Delivery credibility

Customer doubt that a vendor can deliver the full platform as an integrated whole — not just the individual components — is a significant barrier across the sample. High performers have largely closed this gap through more rigorous pilot design, stronger references, and a post-sale experience that produces visible value quickly.

Post-sale value visibility

The largest single performance gap in our data has nothing to do with how companies sell. It is about what happens after the deal closes. On whether customers can easily see the value they are getting after go-live, high performers score 1.86 out of 5 (lower is better on this barrier item), while lower performers score 3.23 — a gap of 1.37 points, larger than any other item in the survey.

This reframes the platform sale in an important way. The behaviors that most directly separate high performers from the rest are not pre-sale. Getting to signature is necessary but not sufficient.

"A lack of perceived value — generally driven by under or improper utilization of the platform." — Survey respondent

Customer-side barriers

Two additional barriers attract broad agreement and affect how the conversation needs to be framed:

- 70% say customers need more peer adoption and proven references before committing. Nobody wants to be first.

- 62% say customers agree they should innovate — but believe now is not the right time. Not active rejection, but indefinite deferral.

The Three Questions Buyers Need Answered

Every barrier we identified maps back to one of the three questions below. Sales organizations that orient their approach around these questions — rather than around features, demos, or ROI models — consistently outperform those that do not.

When any one of these goes unanswered, the deal does not close — it shrinks. Customers ask for something smaller and safer, pilots multiply without converting, and sellers find themselves back in a product sale. Getting back to a platform conversation from there is rare.

Organizing for Complexity

The three questions are not the individual seller's problem alone to solve. The organizations that answer them consistently have built infrastructure that makes it possible — reducing the burden on sellers so they can focus on the work that actually requires human judgment.

High performers invest in four things at the structural level.

1. Getting incentives right

Compensation systems that reward quick wins undermine the platform sale. Sellers measured primarily on quarterly attainment will default to the path of least resistance — which is always the product sale. This is a rational response to how they are measured, not a character failure. Addressing it is a prerequisite, but 46% of respondents acknowledge their incentives are still misaligned.

2. A pilot process that proves the business case

The absence of references is one of the most significant impediments to platform sales. Pilots are the natural answer — but most fail because they end up proving the technology rather than the business case. A technically successful pilot that does not produce measurable business impact does not advance the deal. It delays the same conversation.

High performers design pilots differently:

- Pilots are a scarce resource, not a giveaway. Offered selectively, to customers who have demonstrated genuine strategic intent and organizational readiness.

- KPIs are agreed before the pilot begins, tied to hard outcomes. Revenue, cost reduction, or quantifiable risk — not engagement metrics. The baseline is set in advance so the before-and-after contrast is unambiguous.

- Full implementation is the default, with opt-out rather than opt-in. This disqualifies customers who want a proof of concept but not a genuine transformation — and creates a sense of inevitability that makes the larger commitment feel like a natural next step.

3. A redesigned sales motion

Platform selling requires a more fluid sales motion than most organizations have built. The stages are the same — what happens within them is substantially different.

The biggest shifts are in the middle stages. Explore is about shaping the problem, not just uncovering it. Align is about building a coalition, not managing a single buyer relationship. Both require different conversations and longer time horizons than most product-era sales processes were designed for.

4. Infrastructure for internal coordination

One of the least-discussed differences between high and lower performers is how they coordinate internally around complex deals. Pulling in the right experts at the right time is a persistent weak point — only 39% of companies rate themselves above average at it.

In most organizations, sellers working on a complex deal have to beg and borrow time from colleagues in pre-sales, solution architecture, customer success, and implementation. The coordination that happens depends on personal relationships and goodwill — not process.

"Due to M&A, too many silos — not efficient enough at the moment." — Survey respondent

High performers fix this by creating a formal mechanism for assembling the right internal expertise around deals of sufficient size and complexity — not an additional pipeline review, but a structured forum where deal teams and specialists work through a specific customer opportunity together, using a shared customer value roadmap as the common working document.

This also closes the post-sale gap. The handoff between sales and implementation — one of the most dangerous moments in a platform deal — becomes a continuation of a shared process rather than a cold transfer of ownership.

Individual Behaviors That Distinguish High Performers

Organizational infrastructure creates the conditions. But the sale depends on what individual sellers do in the room.

One finding worth noting upfront: across all nine dimensions, the average self-rating sits between 3.0 and 3.4 out of 5. No single behavior stands out as a clear organizational strength. The gaps between high and lower performers are modest on most pre-sale items — but they open up meaningfully on the post-sale behaviors, consistent with everything else we found.

Three behavioral differences distinguish high performers.

1. Stakeholder mapping before anything else

The instinct in most sales processes is to get to the decision-maker quickly. High performers do something different first: they map the full stakeholder landscape.

Not just the formal buying group — but who is affected by the purchase, who owns the problem, who can veto from outside the room, who might become an informal champion or blocker. They profile individuals: visionary or risk-averse, ally or sceptic, what their track record suggests about how they respond to change.

This is not optional groundwork. Without it, you cannot surface the right risks with the right people, or build a business case that lands with the people who matter.

"Multi-threading, finding mobilisers, being more prescriptive about what a client should do vs. what they want to do." — Survey respondent

2. Raising uncomfortable questions early

The instinct in a complex, high-stakes deal is to present the cleanest possible picture. High performers do the opposite: they surface the awkward questions before the customer does.

The most intractable barriers to platform deals are almost never technical. They are internal to the customer: cultural norms, political relationships, organizational inertia. Sellers who wait for these to surface on their own find them emerging late in the process, when they are hardest to recover from.

"If we've decided there's a need, I'm also going to make sure they address the need," one respondent put it. "If I walk away now, I'm never going to place a solution with them." Surfacing risk early requires both courage and genuine knowledge of what a real implementation involves.

3. A shared business case

The business case is the mechanism through which all three buyer questions get answered in one document: whether it can be done (implementation roadmap and references), whether it is worth it (financial model and cost of inaction), and whether the customer will survive the journey (change management and risk plan).

The critical word is shared. A business case that a seller presents to a buyer is a proposal. One developed together is closer to a commitment. High performers invest in the co-creation process accordingly.

The best business cases go beyond a single-point ROI to present ranges and scenarios — including the cost of doing nothing and the cost of a DIY alternative. In an environment where buyers conduct their own AI-assisted research before every major purchase, an honest range of scenarios is harder to dismiss than a deterministic model.

"When business objectives are known and aligned to the sales message, and the right people are in the room, and the client is properly qualified — our close ratios are phenomenal." — Survey respondent

Conclusions

The platform sale is widely framed as a product problem — a matter of having the right capabilities — or a pricing problem. Our research suggests the real constraint is elsewhere: a gap in sales strategy and organizational capability, specifically the ability to answer three questions that buyers need answered before they will commit to anything more than a proof of concept.

Most organizations describe the value of a full implementation compellingly. But they fail to address the foundational questions around feasibility, impact, and risk — and in the absence of answers, buyers do what any rational actor would do. They ask for something smaller.

The companies that manage this transition invest in the right organizational infrastructure: disciplined pilot design, a redesigned sales motion, aligned incentives, and a formal mechanism for assembling internal expertise around complex deals. Individually, they develop sellers who can navigate complexity rather than just describe their product: who map stakeholders before advancing, surface risks before they surface themselves, and build business cases collaboratively rather than presenting them.

For sales leaders, this reframes the capability agenda. The platform sale does not reward sellers who know more. It rewards sellers who can move across stakeholder groups, connect commercial and operational threads, and hold productive tension with buyers who are skeptical of both the promise and the disruption involved in acting on it.

The stakes for buyers are real. A failed platform implementation can damage a budget and end a career. Sellers who show up prepared to de-risk the decision — rather than just close it — earn a different kind of trust. That trust is what every large platform deal we observed in our research was built on.

How Insight Revenue Can Help

The barriers described in this research are real, but they are not insurmountable. Insight Revenue works with commercial organizations to build the strategy, structure, and individual capabilities needed to win platform deals consistently.

Our work starts with diagnosis. Using the same research framework that underpins this report, we benchmark your organization against peers across the six barrier categories — giving your leadership team a clear picture of where you are navigating well and where you are conceding ground unnecessarily.

From there, we install the BRIDGE Customer Value Roadmap: our structured methodology for managing complex platform deals from first conversation to successful implementation. BRIDGE, which is part of our ´Insight to Value´ sales model, gives sellers, deal teams, and internal experts a shared language and a common process:

- Blueprint the customer's strategy, goals, and stakeholder landscape — before advancing the deal.

- Reframe with insight — introducing perspectives that shift how the customer sees their situation and the cost of staying where they are.

- Illustrate impact — building a business case around the customer's own metrics, including cost of inaction and realistic implementation scenarios.

- Defuse obstacles — surfacing the political, organizational, and operational barriers early, when there is still room to address them.

- Gauge the options — mapping the competitive landscape honestly, including the cost and risk of doing nothing or building in-house.

- Execute a joint plan — a shared roadmap that answers the third foundational question: will we survive the journey?

BRIDGE also provides the structure for the internal coordination forum described in this report. When deal teams work through the roadmap together, the handoff between sales and implementation becomes a continuation of a shared process. Customers experience this as continuity, not a change of ownership.

The result is a commercial organization that does not just sell the platform. It delivers on it.

Download the full report below.